In the 3rd quarter, our organization begins to work with foreign suppliers directly in foreign currency (we opened a foreign currency account, made payments). We need information, step-by-step instructions on payment and accounting for imported goods with types of documents, settlement accounts, setting up contracts in 1C8..

In 1C: Accounting 8, it is necessary to determine the terms of the agreement in the “Agreements” directory. In the “Contract type” field, indicate “with supplier” and select the currency.

To transfer payment to a foreign counterparty, use the document “Outgoing Payment Order”. Operation – “payment to the supplier”, accounting account 52. Accounts for settlements with the supplier and advances – 60.21 and 60.22, respectively.

Please note: it is necessary to fill out the “Currencies” directory in a timely manner in order for the program to correctly calculate ruble amounts and exchange rate differences.

The receipt of goods is documented in the document “Receipt of goods and services”. Operation – “Purchase, commission”. Click the “Price and Currency” button to uncheck the “Take into account VAT” checkbox, because The price of the goods does not include the amount of tax. When filling out the tabular part of the “Products” tab, you must indicate the country of origin and the customs declaration number.

When conducting, the following wires should be formed:

Debit 41.01 Credit 60.21

Goods received at contract price

Debit 60.21 Credit 60.22

Advance credited (if any)

In addition, no correspondence on invoices accounting The corresponding quantity of goods will be credited to the CCD debit (quantitative accounting only).

Reflection of expenses for payment of customs duties and duties specified in the customs declaration is carried out in the document “Customs customs declaration for imports” (main menu - Main activity - Purchasing). On the “Main” tab, the number of the customs declaration and the amount of customs duties are indicated, on the “Sections of the customs declaration” tab - information about material assets and the amount of customs duties.

Debit 41.01 Credit 76.05

The amount of customs duties and customs duties;

Debit 19.05 Credit 76.05

Customs VAT.

Other expenses (for example, customs brokerage services) are reflected in the document “Receipt of additional expenses”.

When conducting, the following transactions are generated:

Debit 41.01 Credit 60.21

Amount of expenses;

Debit 19.04 Credit 60.21

The amount of accrued VAT.

Expenses associated with the acquisition, but not included in the cost of goods, are taken into account in accounts 44, 91 by posting the document “Receipt of goods and services”.

Rationale

On specific example. What postings to make and how to calculate taxes when importing

Example conditions: Progress LLC entered into an import contract

If your company is “simplified”

Companies operating under the simplified regime pay import VAT in the same manner as organizations operating under the general regime. But they cannot deduct tax.

Progress LLC entered into a foreign trade contract. Under this agreement, the company purchases a batch of goods worth 61,000 euros from an Italian supplier. According to the terms of the contract, ownership of the goods passes to the buyer after customs clearance. In July, Progress LLC must pay 30 percent of the cost of goods as an advance payment. The LLC will transfer the rest of the cost of the goods within ten days after their customs clearance.

In July 2012, the advance paid to the supplier is reflected

Progress LLC made an advance payment to the foreign supplier on July 16 in the amount of 18,300 euros (61,000 EUR ? 30%). The Bank of Russia exchange rate on this date is (conditionally) 40.5112 rubles/EUR. The LLC accountant reflected the advance payment with the following posting:

DEBIT 60 subaccount “Settlements on advances issued” CREDIT 52

- 741,354.96 rub. (18,300 EUR ? 40.5112 rubles/EUR) - prepayment was transferred to the seller.

In August 2012, goods received are taken into account

The declaration for imported goods was registered by customs officers on August 2, 2012. The customs value of the goods is equal to the transaction price - 61,000 euros. The exchange rate of the Bank of Russia on the date of customs clearance (conditionally) is 40.6200 rubles/EUR.

When importing goods, the LLC paid a duty of 5 percent of their customs value, that is, 123,891 rubles. (61,000 EUR ? ? 0.6200 rub/EUR) ? 5%). And also customs duty - 5500 rubles.

The amount of VAT paid upon import was RUB 468,307.98. ((61,000 EUR ? 40.6200 rub/EUR + 123,891 rub.) ? 18%).

Important detail

The tax base for import VAT includes the customs value of goods and import duties.

In addition, the LLC paid for the storage of goods, their delivery and loading and unloading. Only 75,000 rubles. According to the accounting policy of Progress LLC, the accountant attributes these expenses to the cost of goods both in accounting and when calculating income tax. In this case, the company partially paid for imported goods. Therefore, the accountant formed the cost of goods based on the amount paid to the supplier as an advance. To it he added the remaining 70 percent of the contractual value of the goods at the exchange rate at the time of transfer of ownership.

So, the accountant reflected the receipt of goods, payment of customs duties and other expenses with the following entries:

DEBIT 76 CREDIT 51

-123,891 rub. - import customs duties have been paid;

DEBIT 76 CREDIT 51

-5500 rub. - customs duty is transferred;

DEBIT 68 subaccount “VAT calculations” CREDIT 51

-468,307.98 rub. - “import” VAT has been paid;

DEBIT 19 CREDIT 68 subaccount “VAT calculations”

-468,307.98 rub. - reflected VAT paid;

DEBIT 76 CREDIT 51

-75,000 rub. - payment for storage, delivery, loading and unloading of goods is listed;

DEBIT 41 CREDIT 60 subaccount “Payments for goods”

-2,475,828.96 rub. (741,354.96 rub. + (61,000 EUR ? 70% ? ? 40.6200 rub/EUR)) - received goods are taken into account;

DEBIT 60 subaccount “Payments for goods” CREDIT 60 subaccount “Settlements for advances issued”

-RUB 741,354.96 - advance payment paid to the supplier is credited;

DEBIT 41 CREDIT 76

-204,391 rub. (123,891 + 5,500 + 75,000) - the cost of goods includes customs duties and customs fees, storage costs, delivery and loading and unloading;

DEBIT 68 subaccount “VAT calculations” CREDIT 19

-468,307.98 rub. - paid “import” VAT is accepted for deduction.

On the date of payment for goods, the exchange rate difference is determined

Progress LLC transferred payment to the supplier in the amount of 70 percent of the cost of goods on August 7, 2012. The exchange rate for this date (conditionally) is 41.7235 rubles/EUR. The accountant determined the exchange rate difference and compiled an accounting certificate (see below).

The accountant made the following entries in accounting:

DEBIT 60 CREDIT 52

-1,781,593.45 rub. (61,000 EUR ? 70% ? 41.7235 RUR/EUR) - the remaining payment for the goods is transferred;

DEBIT 91 subaccount “Other expenses” CREDIT 60

-47,119.45 rub. (61,000 EUR ? 70% ? (41.7235 rub/EUR – – 40.6200 rub/EUR)) - negative exchange rate difference is taken into account.

In tax accounting, the accountant included this exchange rate difference in non-operating expenses.

How to get a deduction for VAT paid at customs upon import, what date should be indicated on the customs declaration upon receipt imported goods the article will tell.

Question: What date should the customs declaration be carried out if the release date differs from the date in the goods declaration. The date of receipt of imported goods is the date of release according to the TD, because the contract with the foreign supplier stipulates that the transfer of ownership of the goods passes from the moment the goods are released into free circulation on the territory of the Russian Federation, specific date in the customs mark “Release is allowed”, but the DT was drawn up on a different date and the $ exchange rate is different. It turns out that I arrive according to the date of the stamp “Issuance is permitted”, and what date should the GDT be carried out? Posting date or DT date, is the $ exchange rate different for each date?

Answer: You do not need to carry out customs declaration in accounting at all.

You are obliged to receive the goods according to the terms of the contract - on the date of the customs mark “Release allowed”. The date of compilation of the customs declaration does not play any role for accounting purposes.

How to get a deduction for VAT paid at customs upon import

Situation: at what point does the right to deduct VAT paid at customs upon import arise?

The right to deduct VAT paid at customs arises in the quarter when the imported goods were accepted for registration and is retained by the importer for three years from that moment. For example, if goods were accepted for accounting on June 30, 2016, then the right to deduct VAT paid at customs when importing these goods remains with the buyer until June 30, 2019 (Clause 3, Article 6.1 of the Tax Code of the Russian Federation).

VAT paid at customs can be deducted if the following conditions are met:

- the goods were purchased for transactions subject to VAT or for resale;

- the goods are credited to the organization’s balance sheet;

- the fact of payment of VAT is confirmed.

VAT is deductible if the imported goods were placed under one of four customs procedures:

- release for domestic consumption;

- processing for domestic consumption;

- temporary importation;

- processing outside the customs territory.

This procedure for applying the deduction follows from the provisions of paragraphs, Article 171 and paragraphs, 1.1 of Article 172 of the Tax Code of the Russian Federation.

The organization’s own property and all business transactions performed by it are reflected in the corresponding accounting accounts (clause 3 of Article 10 of the Law of December 6, 2011 No. 402-FZ). Thus, acceptance for accounting is a reflection of the value of property on the accounting accounts that are intended for this purpose.

If we're talking about about inventory items, registration is the moment when their value is reflected in account 10 “Materials” or account 41 “Goods” with the execution of the corresponding primary documents (for example, a receipt order in form No. M-4, a consignment note in the form No. TORG-12). This conclusion is confirmed by the Russian Ministry of Finance in a letter dated July 30, 2009 No. 03-07-11/188.

Deduction of VAT amounts paid upon import of fixed assets, equipment for installation and (or) intangible assets, is carried out in full after they are registered (clause 1 of article 172 of the Tax Code of the Russian Federation).

When registering imported goods, it is necessary to take into account the features associated with determining the moment of transfer of ownership of goods from the seller to the buyer. This moment (for example, shipment of goods to the carrier, payment for goods by the buyer, crossing of the Russian border by goods, etc.) must be recorded in foreign trade contract. If there is no such clause, the date of transfer of ownership should be considered the moment the seller fulfills his obligation to supply the goods. Usually this point is associated with the transfer of risks from the seller to the buyer, which in turn is determined by the provisions International rules interpretation of trade terms "INCOTERMS 2010".

If imported goods have been cleared through customs, but ownership of them has not yet transferred to the buyer, they can be taken into account off the balance sheet. For example, on account 002 “Inventory assets accepted for safekeeping.” In this case, the buyer also has the right to deduct VAT paid at customs. This conclusion can be drawn from the letters

More and more companies are purchasing goods abroad and subsequently selling them on the domestic market of the Russian Federation. Therefore, issues of accounting and tax accounting for the import of goods do not lose their relevance. Main issues of import of goods in 2018/2019 Let's look at it in our article.

How is the cost of imported goods determined?

As you know, goods are accepted for accounting at actual cost (clause 5 of PBU 5/01). It is important to note that when importing goods, as a rule, additional expenses in the form of customs duties, fees, and other payments paid to intermediaries for customs clearance of goods. All these expenses are also included in the cost of imported goods (clause 6 of PBU 5/01).

No less important is the correct determination of the accounting value of goods under an agreement with a foreign supplier, i.e., the conversion into rubles of the cost of goods expressed in foreign currency. Let us remind you that the cost of goods is reflected in rubles at the rate in effect on the date of their acceptance for accounting (clause 6, clause 9 of PBU 3/2006). If goods are purchased against a previously transferred prepayment to the supplier, the cost of the goods is fixed at the rate in effect on the date of the prepayment, and in the part not covered by the prepayment - at the rate at which the goods are accepted for registration. Read separate material on the peculiarities of forming the ruble valuation of acquired values under contracts in foreign currency, including on account.

Tax accounting for import of goods

The procedure for forming the actual cost of imported goods in tax accounting is similar to that discussed above. At the same time, it is advisable for the organization to fix the specific composition of expenses taken into account in the cost of purchased goods in its accounting policy for tax purposes (clause 3, clause 1, article 268 of the Tax Code of the Russian Federation).

Accounting for import of goods: example in postings

On December 5, 2018, the organization purchased a consignment of goods with a contract value of $10,000. Title to the goods transferred on the same day. The customs fee is 15,000 rubles. Customs duty - 15%. The calculated VAT at customs at the rate as of December 5, 2018 amounted to RUB 137,545. (10,000 * 66.4467 * 1.15 * 0.18). Intermediary services for customs clearance RUB 141,600. incl. VAT 18%. Payment for the goods was made in full on December 11, 2018. US dollar exchange rate as of 12/05/2018 - 66.4467, as of 12/11/2018 - 66.2416.

| Operation | Account debit | Account credit | Amount, rub. |

|---|---|---|---|

| 12/05/2018 imported goods were registered (10 000 * 66,4467) | 41 "Products" | 60 “Settlements with suppliers and contractors” | 664 467 |

| Customs VAT calculated | 19 “VAT on purchased assets” | 76 “Settlements with various debtors and creditors” | 137 545 |

| Customs duty on imported goods reflected | 41 | 76 | 15 000 |

| The customs duty on imported goods is reflected (10,000 * 66.4467 * 0.15) | 41 | 76 | 99 670 |

| The services of an intermediary for customs clearance of imported goods are reflected | 41 | 60 | 120 000 |

| VAT on intermediary services included | 19 | 60 | 21 600 |

| VAT is accepted for deduction (137 545 + 21 600) | 68 “Calculations for taxes and fees” | 19 | 159 145 |

| 12/11/2018 debt for imported goods was paid (10 000 * 66,2416) | 60 | 52 “Currency accounts” | 662 416 |

| The exchange rate difference in settlements with a foreign supplier is reflected (10 000 * (66,2416 — 66,4467)) | 60 | 91 “Other income and expenses”, subaccount “Other income” | 2 051 |

VAT paid at customs is deducted after imported goods are registered (

This information will be useful to organizations importing goods into the territory Russian Federation. In this article we will tell you about accounting import operations, we will give an accessible explanation of the features of accounting, tax accounting, and the formation of the cost of imported goods, supported by the regulatory framework.

Accounting for import transactions

In accordance with the Federal Law of December 8, 2003 No. 164-FZ “On the Fundamentals of State Regulation of Foreign Trade Activities” (as amended and supplemented) (clause 10 of Article 2), import of goods is the import of goods into the Russian Federation without the obligation to re-export .

To avoid problems with legislation, it is necessary to very scrupulously maintain both accounting and tax records of import transactions.

Accounting for import transactions is in many ways similar to tax accounting, but there are a number of distinctive features:

Accounting entries for accounting for import transactions

Details about accounting and tax accounting Import transactions will be explained further:

| Accounting entry | Explanation | Document confirming the operation | |

| D 60 | K 52 | Transfer of advance payment to the supplier for imported goods | Bank statement, payment order |

| D 76 | K 51 | Payment of customs duties | DT, bank statement, payment order |

| D 07 | K 60 |

| Form No. OS-14 “Act of acceptance (receipt) of equipment” Form No. MX-1 “Act of acceptance and transfer of goods” material assets for storage" Form TORG-1 “Act of acceptance of goods” |

| D 19 | K 76 | Import VAT reflected | DT, bank statement, accounting certificate |

| D 07 | K 60 | Accounting information | |

| D 19 | K 60 | Invoices, accounting certificates | |

| D 01 | K 08-4 | Form No. OS-1 “Act of acceptance and transfer of fixed assets (except for buildings, structures)” | |

| D 68 | K 19 | Submitting import VAT for deduction | Invoice, accounting certificate |

| D 60 | K 91-1 | Accounting information | |

| D 91-2 | K 60 | Accrual of negative exchange rate differences on settlements with suppliers in foreign currency | Accounting information |

| D 60 | K 52 | Bank statement | |

Tax accounting of import transactions

According to paragraph 3 of paragraph 1 of Article 268 of the Tax Code of the Russian Federation, when selling property or property rights, the taxpayer has the right to reduce income from such transactions by the amount of expenses directly related to such sale. The following expenses are taken into account:

- at the rate;

- storage;

- service;

- transportation.

In accordance with Article 320 of the Tax Code of the Russian Federation, the procedure for determining expenses for trade operations is determined. According to this normative act The amount of distribution costs includes expenses for:

- delivery of goods;

- warehousing costs;

- other expenses associated with the purchase of goods.

The taxpayer has the right to determine the cost of goods taking into account distribution costs. The formation of the cost of goods is explained in detail in the section “How is the cost of imported goods formed?”.

Example of accounting for import transactions

ABC LLC purchased goods in Spain for the amount of €8,000 on July 11, 2017. ABC LLC received property rights to the goods on July 11, 2017.

- Customs duty – 12,000 rubles.

- Customs duty – 15%.

- Calculated VAT: 8000*68.77*1.15*0.18=113883.12 rubles.

- Costs for delivery of property to the territory of the Russian Federation 34650.00 (including VAT 6237.00)

On July 16, 2017, the final payment for the goods was made. € exchange rate: 07/11/2017 – 68.77 rubles, 07/16/2017 – 68.36 rubles.

| Accounting entry | Explanation | Amount (rub.) | |

| D 76 | K 51 | Payment of customs duties | 12 000,00 |

| D 76 | K 51 | Payment of customs duties | 82 524,00 (8000*68,77*0,15) |

| D 07 | K 60 | Ownership rights to goods as:

The owner accepts independent decision, guided by regulations. | 550 160,00 (8000*68,77) |

| D 19 | K 76 | Import VAT reflected | 113 883,12 |

| D 07 | K 60 | Costs of delivering property to the territory of the Russian Federation | 34 650,00 |

| D 19 | K 60 | VAT on property transportation | 6 237,00 |

| D 01 | K 08-4 | Capitalization of received property | 550 160,00 |

| D 68 | K 19 | Submission for VAT deduction | 120 120,12 (113 883,12+6237) |

| D 60 | K 91-1 | Accrual of positive exchange rate differences on settlements with suppliers in foreign currency | 3 280,00 (8000*(68,77-68,36)) |

| D 60 | K 52 | Final payment to the supplier for the imported goods | 546 880,00 (8 000*68,36) |

Errors in accounting for import transactions

When accounting for import transactions, you must be very careful to avoid errors that are often identified during an audit:

- incorrect conversion of foreign currency into rubles when conducting a foreign exchange transaction;

- there is no translation into Russian of the text of the document on the basis of which payment is made from a foreign currency account;

- failure to comply with deadlines for fulfilling obligations under contracts providing for advance payments;

- incorrect correspondence of invoices for accounting of import transactions.

How is the cost of imported goods determined?

In accordance with clause 6 of the Accounting Regulations “Accounting for Inventories” PBU 5/01,” the actual cost of inventories acquired for a fee is recognized as the amount of the organization’s actual costs for the acquisition, excluding value added tax and other reimbursable taxes (except for cases provided for by the legislation of the Russian Federation). To determine the actual cost, you can use the following formula:

Actual costs:

- amounts paid in accordance with the agreement to the supplier (seller);

- amounts paid to organizations for information and consulting services related to the acquisition of inventories;

- customs duties;

- non-refundable taxes paid in connection with the acquisition of a unit of inventory;

- remunerations paid to the intermediary organization through which inventories were acquired;

- costs for the procurement and delivery of inventories to the place of their use, including insurance costs. These costs include, in particular, costs for the procurement and delivery of inventories;

- costs of maintaining the procurement and warehouse division of the organization, costs of transport services for the delivery of inventories to the place of their use, if they are not included in the price of inventories established by the contract; accrued interest on loans provided by suppliers (commercial loan); interest on borrowed funds accrued before the inventory was accepted for accounting, if it was raised for the acquisition of these inventories;

- costs of bringing inventories to a state in which they are suitable for use for the intended purposes. These costs include the organization’s costs for part-time work, sorting, packaging and improvement technical characteristics inventories received that are not related to the production of products, performance of work and provision of services;

- other costs directly related to the acquisition of inventories.

General and other similar expenses are not included in the actual costs of purchasing inventories, except when they are directly related to the acquisition of inventories.

Clause 6 states that conversion into rubles is made at the rate valid on the date of the transaction in foreign currency. According to clause 9 of PBU 3/2006, in case of making an advance payment for the purchased goods exchange rate fixed on the date of prepayment with the establishment of the corresponding cost of the goods. The remaining part of the goods will be accepted for accounting, taking into account the changed exchange rate (if such a phenomenon occurs).

Documents required for registration of imported goods

According to the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” (Article 9), each fact economic activity must be subject to registration as a primary accounting document. To account for import transactions, the primary accounting documents, the presence of which is necessary for accounting and tax accounting of imported goods, are:

- foreign trade contract with the importer of goods;

- invoice issued by the seller;

- transport, forwarding documents;

- insurance documents;

- declaration of goods (DT);

- bank certificates confirming payment of customs duties and duties;

- invoices, acts of acceptance of inventory items;

- technical documentation. Read also the article: → "".

Legislative acts regulating the import of goods:

| Normative act | Regulatory area |

| Order of the Ministry of Finance of the Russian Federation dated June 9, 2001 No. 44n “On approval of the accounting regulations “Accounting for inventories” PBU 5/01” (with amendments and additions) | Formation of the cost of imported goods |

| Order of the Ministry of Finance of the Russian Federation dated November 27, 2006 No. 154n “On approval of the Accounting Regulations “Accounting for assets and liabilities, the value of which is expressed in foreign currency” (PBU 3/2006)” (with amendments and additions) | Determining the cost of goods depending on the exchange rate |

| clause 3 clause 1 article 268 of the Tax Code of the Russian Federation | Tax accounting of imported goods |

| Article 320 of the Tax Code of the Russian Federation | The procedure for determining expenses for trading operations |

| According to the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” (Article 9) | Primary accounting documents |

| Federal Law of December 8, 2003 No. 164-FZ “On the Fundamentals of State Regulation of Foreign Trade Activities” (Clause 10, Article 2) | Definition of import of goods |

Category “Questions and Answers”

Question No. 1. Are we required to make advance payments to a foreign seller when purchasing imported goods?

The obligation to pay an advance payment arises provided that this obligation appears in the contract that you have concluded with the foreign supplier. If the contract does not provide for an advance payment when purchasing imported goods, you are not obliged to pay it.

Question No. 2. Do I understand correctly that Accounting goods begins on the day of transfer of property rights to it, even if the goods have not yet been received and paid for?

Yes, in accordance with the legislation of the Russian Federation, the buyer of imported goods accepts the goods for fixed assets or inventories at the time of transfer of property rights from the seller.

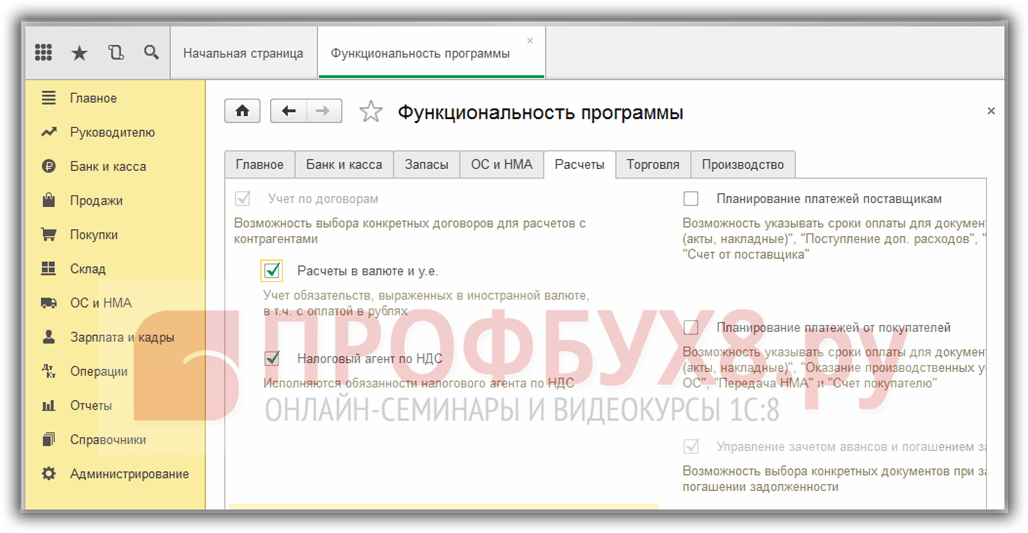

Step 1. Settings for accounting for imported goods according to the customs declaration

It is necessary to configure the functionality of 1C 8.3 through the menu: Home- Settings – Functionality:

Let's go to the bookmark Reserves and check the box Imported goods. After installing it in 1C 8.3, it will be possible to keep track of batches of imported goods by customs declaration numbers. The details of the customs declaration and the country of origin will be available in the receipt and sale documents:

To carry out settlements in foreign currency, on the Calculations tab, check the Settlement in foreign currency and monetary units checkbox:

Step 2. How to capitalize imported goods in 1C 8.3 Accounting

Let's enter the document Receipt of goods in 1C 8.3 indicating the customs declaration number and country of origin:

The movement of the receipt document will be as follows:

By debit of the auxiliary off-balance sheet account gas turbine engine information will be displayed on the quantity of imported goods received, indicating the country of origin and the customs declaration number. The balance sheet for this account will show the balances and movement of goods in the context of the customs declaration.

When selling imported goods, it is possible to control the availability of goods moved under each customs declaration:

In the 1C 8.3 Accounting program on the Taxi interface for accounting for imports from member countries of the customs union, changes have been made to the chart of accounts and new documents have appeared. For more information about this, watch our video:

Step 3. How to account for imported goods as assets in transit

If during the delivery period it is necessary to take into account imported goods as material assets in transit, then you can create additional warehouse for accounting of such goods as warehouse Goods are shipping:

Account 41 analytics can be configured by storage location:

To do this, in 1C 8.3 you need to make the following settings:

Click on the Inventory Accounting link and check the box By warehouses (storage locations). This setting in 1C 8.3 makes it possible to enable analytics of the storage location and determine how accounting will be kept: only quantitative or quantitative-cumulative:

When goods actually arrive, we use the document to change the storage location:

Let's fill out the document:

The balance sheet for account 41 shows movements in warehouses:

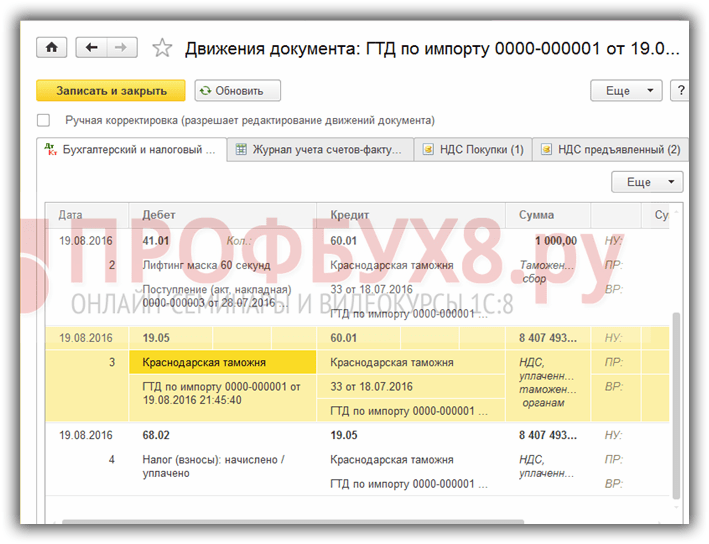

Step 4. Filling out the customs declaration document for import in 1C 8.3

Enterprises that carry out direct deliveries of imported goods must reflect customs duties for the received goods. Document Customs declaration for import into 1C 8.3 can be entered based on the receipt document:

or from the Purchases menu:

Let's fill out the customs declaration document for import into 1C 8.3 Accounting.

On the Main tab we indicate:

- The customs authority to which we pay duties and the contract, respectively;

- On what gas customs declaration number the goods have arrived;

- Amount of customs duty;

- The amount of fines, if any;

- Let's put up a flag Record the deduction in the purchase book, if you need to reflect it in the Purchase Book and automatically deduct VAT:

On the Customs Declaration Sections tab, enter the amount of the duty. Since the document was generated on the basis, 1C 8.3 has already filled in certain fields: customs value, quantity, batch document and invoice value. Let's enter the amount of duty or the % duty rate, after which 1C 8.3 will distribute the amounts automatically:

Let's review the document. We see that customs duties are included in the cost of goods:

Study in more detail the features of the receipt of goods in the event that the supplier’s SF indicates a customs declaration, check the registration of such SF in the Purchase Book, study the 1C 8.3 program for professional level with all the nuances of tax and accounting, from the correct entry of documents to the generation of all basic reporting forms - we invite you to our. For more information about the course, watch our video: